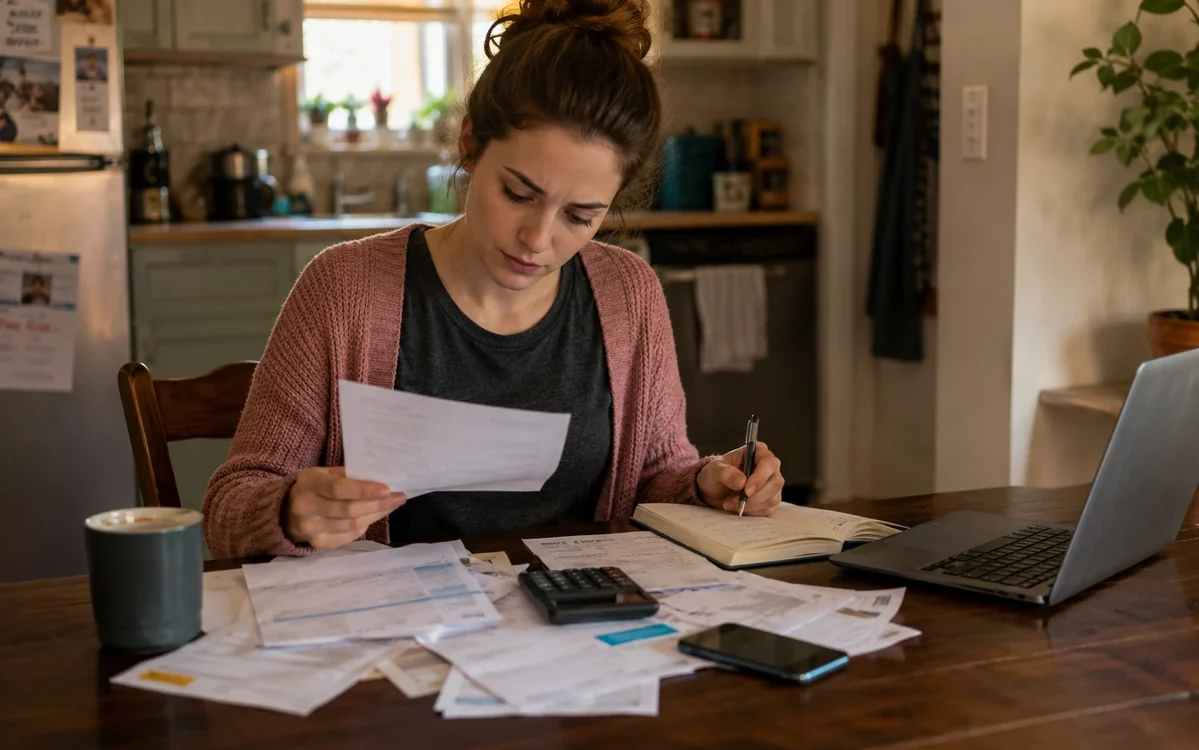

Recurring bills are sneaky because they do not feel like decisions anymore. You made the decision once, months or years ago, and now the money just leaves every month like it owns the place.

That is exactly why companies love auto-renewal. They know most people will complain about a $9 grocery price increase, then ignore a $17 internet bill increase because it shows up quietly in the background. A budget does not usually break from one dramatic mistake. It gets worn down by little charges that nobody rechecks.

I am not against auto-pay. Auto-pay keeps bills from being late, which is useful. But auto-renewal without review is where the trouble starts. Once or twice a year, I go through the bills below and ask one simple question: would I choose this plan again today at this price?

1. Internet service

Internet companies are masters of the quiet price climb. The first year looks reasonable, then the promotional rate expires, fees appear, equipment rental gets added, and suddenly the same service costs more for no good reason beyond corporate imagination.

Before letting it renew, check your current speed, your actual usage, and the price new customers are being offered. If your household mostly streams, browses, emails, and uses a few devices at once, you may not need the top-tier plan. Faster is not always better if you are paying for speed you never use.

Look at the equipment fee too. Renting a modem or router can quietly cost more than buying your own compatible equipment. That does not mean buying is always the right move, but it is worth doing the math before donating another year of rental fees to the internet gods.

Faye's quick move: Search your provider's current offers before you call. If new customers are getting a better deal, you have something concrete to ask about instead of just vaguely hoping they feel generous. They probably will not. Companies are not golden retrievers.

2. Cell phone plans

Cell phone bills are another place where old plans hang around long after they stop making sense. You may be paying for more data than you use, extra lines you barely need, device protection you forgot about, or a premium plan that sounded responsible three phones ago.

Start by checking your actual data usage for the last three months. Not what you think you use. What you actually use. Plenty of people pay for unlimited data while using less than a cheaper plan would include.

Then check smaller carriers, prepaid plans, family plans, and senior plans if they apply. The big-name plan is not automatically better. Sometimes it is just familiar, and familiarity is one of the most expensive words in personal finance.

3. Car insurance

Car insurance is easy to ignore because the bill feels official. It has policy numbers and coverage language and the emotional warmth of a printer manual. But the price can change for reasons that have nothing to do with your personal driving.

Before renewal, review your coverage, deductibles, mileage, listed drivers, and discounts. If you drive less than you used to, work from home, moved, paid off the car, added safety features, or bundled policies, your old setup may not match your current life.

It is also worth getting quotes from a few other insurers at least once a year. You do not have to switch every time. The point is to know whether your current company is still competitive or just charging you the loyal-customer tax, which is apparently the reward for not being annoying enough.

4. Homeowners or renters insurance

Home and renters insurance should not be set once and forgotten forever. Your belongings change, local risks change, deductibles change, and policy pricing can creep up while you are busy living your life like a normal person instead of reading insurance declarations for sport.

For renters insurance, make sure you are not overpaying for a policy bundled into something else or missing a cheaper option through your auto insurer. For homeowners insurance, check your deductible, coverage limits, roof details, security discounts, and whether your policy still reflects the home accurately.

The goal is not to strip coverage down to the cheapest possible version. That is how people save $11 and create a $9,000 problem later. The goal is to make sure you are paying for the right protection, not stale assumptions.

5. Streaming subscriptions

Streaming started as the cheaper alternative to cable, then everyone launched their own app and we collectively rebuilt cable with worse menus. A few services can be worth it. A pile of forgotten services is just digital clutter with a billing department.

Look at what you actually watched in the last month. If a service has not been opened, pause it. If you only keep it for one show, cancel after the season ends. If a bundle includes services nobody uses, question the bundle instead of letting the word "bundle" hypnotize you.

This is one of the easiest categories to rotate. You do not need every service every month. Keep the one or two you are actively using, then switch when there is something specific you want to watch.

6. Credit card annual fees

Some credit card annual fees are worth paying. Many are not. The problem is that people remember the exciting sign-up bonus and forget to review the card once the normal yearly fee arrives.

Before the fee posts, add up the benefits you actually used: statement credits, travel perks, insurance protections, free checked bags, cash back, points value, and purchase protections. Be honest. A benefit you planned to use but did not use is worth exactly zero dollars, which is rude but mathematically committed.

If the card no longer earns its fee, call and ask about a retention offer or a no-fee downgrade option. Closing a card is not always the best move because it can affect your credit history and available credit, but paying for unused perks is not exactly genius behavior either.

7. Local services and maintenance plans

This category includes pest control, lawn care, pool service, home security, HVAC maintenance plans, cleaning services, storage units, and any other recurring local bill that quietly renews because nobody wants to deal with it.

These services often start for a specific reason. Then the reason fades, but the bill stays. Maybe the pest problem is gone. Maybe the storage unit is full of things you would not buy again for $20. Maybe the home security plan includes equipment you already paid off years ago.

Before renewal, ask what the service includes, how often it is actually being used, whether the price has increased, and whether another local provider offers the same service for less. For maintenance plans, check whether the included visits and discounts are actually worth more than the annual fee.

How to do a bill review without making it miserable

You do not need a spreadsheet with fourteen tabs and the emotional energy of a tax audit. Just open your bank or credit card statement and write down every recurring charge from the last month.

For each one, mark it as keep, cancel, compare, or renegotiate. That is it. Do not overcomplicate this into a new hobby, because then you will avoid it and nothing gets fixed.

- Keep: The price is fair and you still use it.

- Cancel: You forgot about it or no longer need it.

- Compare: You still need the service, but the price feels high.

- Renegotiate: You want to stay, but not at the current rate.

The biggest wins usually come from the boring bills: internet, insurance, phone plans, and local services. Subscriptions matter too, but saving $8.99 is not the same as cutting $35 off a monthly bill you have ignored for three years.

What to say when you call

Do not over-explain. You are not pleading your case before a financial tribunal. Keep it simple:

Try this: "I'm reviewing my monthly bills and noticed my rate has gone up. I like the service, but I'm comparing options. Are there any current promotions, loyalty discounts, or lower-cost plans available?"

If the first person cannot help, ask whether there is a retention or loyalty department. Be polite, but do not be mushy about it. Your goal is not to become best friends with customer service. Your goal is to stop overpaying.

The bottom line

Auto-pay is useful. Auto-renewal without review is expensive. There is a difference.

Pick one afternoon twice a year and check the bills that keep coming back. You may find nothing. More likely, you will find at least one old plan, one unused service, one expired promotion, and one company that has been charging you extra because you were too busy to notice.

That is not a character flaw. That is exactly how the system is designed. The fix is not dramatic. It is just looking at the bill before it renews and making the company re-earn your money.

This connects closely with 15-minute monthly money check-in. It also fits with quiet money leaks that are easy to miss, because the same small decisions tend to overlap in real life.