I used to think money leaks had to be dramatic. A giant bill. A broken appliance. A mysterious charge from some company with a name that sounded like it was assembled by a spam bot.

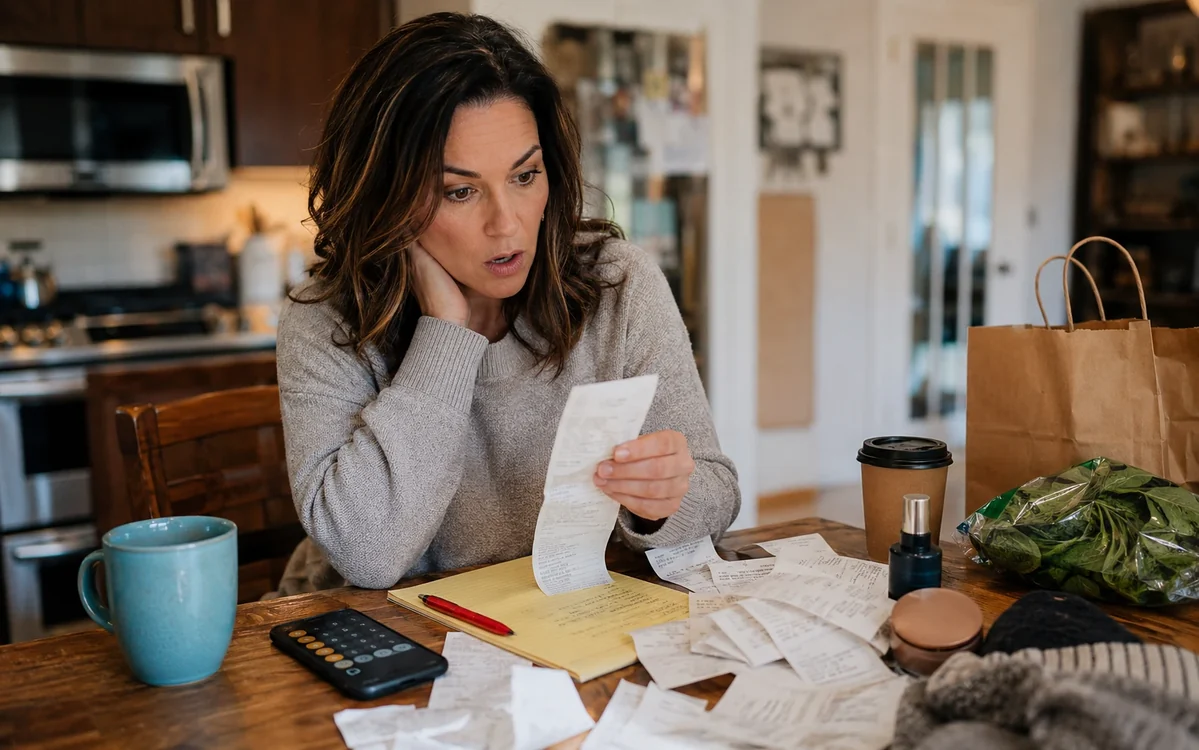

Then I checked one normal month of spending and realized the problem was much sneakier. I didn’t have one big leak. I had a dozen tiny ones, each wearing a fake mustache and pretending to be harmless.

None of these were life-ruining purchases on their own. That was the annoying part. They were small, forgettable, and easy to justify in the moment. But added together, they explained why my checking account kept looking personally offended by the end of the month.

Faye’s rule: If I need to go back to the store for one thing, I write it down and wait unless it is urgent. The store is not a building. It is a trap with fluorescent lighting.

1. The extra grocery trips

My planned grocery trip was not the problem. The problem was the little “I’ll just run in for one thing” trips afterward. Somehow one missing onion became a receipt with coffee creamer, crackers, paper towels, and a seasonal candle I apparently needed for emotional infrastructure.

The leak was not groceries. It was unplanned grocery trips. A second or third trip in the week gave me more chances to impulse-buy things that were never on the original list.

2. Delivery fees and tips

Delivery is convenient, and sometimes it is worth it. But when I looked at the month honestly, I wasn’t just paying for dinner. I was paying delivery fees, service fees, tips, menu markups, and the privilege of eating fries that had lost the will to live.

The real cost was bigger than the meal. One delivery order did not look terrible. Several in a month looked ridiculous.

3. Subscriptions I forgot about

A few dollars here, a few dollars there, and suddenly I was apparently sponsoring half the internet. Streaming trials, app upgrades, cloud storage, a fitness thing I opened twice, and one subscription I had no memory of signing up for because apparently past-me cannot be trusted with a free trial.

Forgotten subscriptions are quiet because they are designed to be quiet. They hit automatically, usually for an amount just small enough that you don’t stop and investigate.

Faye’s rule: If I forgot I was paying for it, the subscription has already made its argument against itself.

4. The “while I’m here” purchases

This was one of the worst offenders because it felt so reasonable. I was already at the store. I already needed something. So why not grab socks, storage bins, a new cleaner, and a pack of pens even though my house already contains enough pens to supply a courthouse?

Convenience spending hides inside legitimate errands. The errand may be necessary. The extras usually are not.

5. Paying for convenience twice

This one irritated me because it felt especially preventable. I would buy pre-cut produce because I was tired, then still order food later because I did not actually cook. Or I would pay for a convenience service and then not use the time it supposedly saved for anything useful.

If convenience does not change the outcome, it is just a surcharge. Paying extra is fine when it actually solves the problem. It is not fine when it only makes the receipt fancier.

6. Premium versions I didn’t need

I found a pattern where I kept choosing the nicer version by default. The premium app plan. The better paper towels. The name-brand pantry item. The upgraded shipping. None of it felt extravagant. That is how it got away with it.

Small upgrades feel harmless because they are small. But a month full of tiny upgrades can quietly become a category of its own.

7. Unused memberships

Memberships are sneaky because they feel like a smart-person decision at the beginning. Join, save money, get access, feel organized. Then real life happens, and suddenly the membership is still billing while you are not using it enough to justify the fee.

A membership only saves money if your actual behavior matches the plan. Not your ideal behavior. Not your January behavior. Your real, Tuesday-night, tired-person behavior.

8. Little home things that weren’t urgent

I like making the house feel better, so this category annoyed me because it was not all waste. A better towel, a nicer basket, a lamp shade that does not make the room look like a DMV lobby — those can be good purchases.

The leak was buying too many small home things without a plan. Individually cute does not mean collectively smart. The house does not need a constant trickle of tiny improvements to be livable.

9. Replacement purchases caused by disorganization

This one was embarrassing, which means it was probably useful. I found myself rebuying things I already owned because I could not find them: tape, batteries, medicine, cleaning supplies, charging cords. Nothing says financial excellence like buying a second pack of something hiding six feet away in a drawer.

Clutter can turn into duplicate spending. Sometimes the cheapest thing you can do is organize one annoying cabinet before buying anything else.

Faye’s rule: If organizing a drawer prevents me from rebuying something, that drawer just paid rent.

10. The small emotional purchases

Not all emotional spending is bad. Sometimes a coffee, a magazine, or a new candle is cheaper than fully losing your mind in public, and we should respect practical solutions.

But my spending check showed a pattern: little purchases used as tiny rewards for being tired, annoyed, bored, or overwhelmed. The problem was not the treat. The problem was using buying as the default reset button.

The bottom line

The point of checking one month of spending is not to shame yourself into becoming a joyless spreadsheet goblin. The point is to see what your money is doing when you are not paying attention.

For me, the biggest lesson was simple: the leaks were not always bad decisions. A lot of them were rushed decisions, tired decisions, automatic decisions, and “it’s only a few dollars” decisions.

If you check your own month of spending, look for the patterns, not just the purchases. One coffee is not the issue. Ten convenience buys, three forgotten subscriptions, and four unplanned store trips might be.

If you have a money leak you found the hard way, tell me. I genuinely like hearing the little traps other people have caught, mostly because it makes me feel less personally targeted by receipts.

This connects closely with 15-minute monthly money check-in. It also fits with unexpected expenses I finally started saving for, because the same small decisions tend to overlap in real life.